Worldwide PC shipments totaled 71.4 million units in the third quarter of 2020, a 3.6% increase from the third quarter of 2019, according to preliminary results by Gartner, Inc. Consumer demand for PCs due to home entertainment and distance learning needs during the ongoing pandemic, along with the strongest growth the U.S. PC market has seen in 10 years, drove the global market momentum.

“This quarter had the strongest consumer PC demand that Gartner has seen in five years,” said Mikako Kitagawa, research director at Gartner. “The market is no longer being measured in the number of PCs per household; rather, the dynamics have shifted to account for one PC per person. While PC supply chain disruptions tied to the COVID-19 pandemic have been largely resolved, this quarter saw shortages of key components, such as panels, as a result of this high consumer demand.

“The business PC market had a more cautious dynamic this quarter. Businesses have continued to buy PCs for remote work, but the focus has shifted from urgent device procurement towards cost optimization. However, enterprise spending remained strong where government funding for distance learning and remote work has fueled device purchases, such as in the U.S. and Japan.”

While Gartner does not include Chromebook shipments in its traditional PC market results, Chromebook shipments grew by approximately 90% in the third quarter of 2020, compared to a year ago. This demand was driven by distance learning due to the pandemic, especially in the U.S. education market. Including Chromebooks, the total worldwide PC market grew around 9% year over year, with Chromebooks representing about 11% of the combined PC/Chromebook market.

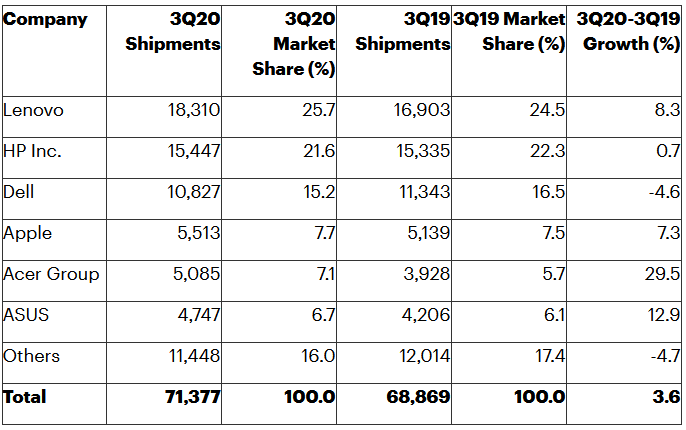

The top three vendors in the traditional PC market remained unchanged from the previous quarter, although Lenovo widened its lead over HP after a quarter of record shipment volume. Consumer-oriented vendors such as Apple, Acer and Asus saw growth that outpaced the rest of the market in the third quarter of 2020 (see Table 1).

Table 1. Preliminary Worldwide PC Vendor Unit Shipment Estimates for 3Q20 (Thousands of Units)

Notes: Data includes desk-based PCs, notebook PCs and ultramobile premiums (such as Microsoft Surface), but not Chromebooks or iPads. All data is estimated based on a preliminary study. Final estimates will be subject to change. The statistics are based on shipments selling into channels. Numbers may not add up to totals shown due to rounding.

Source: Gartner (October 2020)

Lenovo maintained its No. 1 position in the worldwide PC market, with quarterly shipments rising to over 18 million units for the first time ever. Similar to other vendors, Lenovo experienced a decline in desktop shipments, but the decline was not as steep as those experienced by HP and Dell, as Lenovo’s desktop demand was supported by solid growth in China.

HP saw below-market growth as desktop shipments declined 30% year over year, resulting in a growth of just 0.7% in the third quarter of 2020. HP performed relatively well in the U.S. market where shipments grew faster than the regional average, but experienced challenges in Asia Pacific and Japan. HP also announced in August 2020 that the company had a strong backlog in notebooks due to continued supply chain constraints from the pandemic, which limited shipments for the quarter. HP had a strong focus on Chromebooks, remaining the top vendor in this segment.

Dell’s streak of 17 consecutive quarters of year over year growth ended this quarter with a 4.6% decline, reflecting its focus on business over consumer PCs. Dell’s mobile PC sales grew, but steep declines in desktop PC sales offset this growth. Dell’s decline is one indicator of cautious spending by business buyers as a reaction to the current weak economies in most developed nations.

Regional Overview

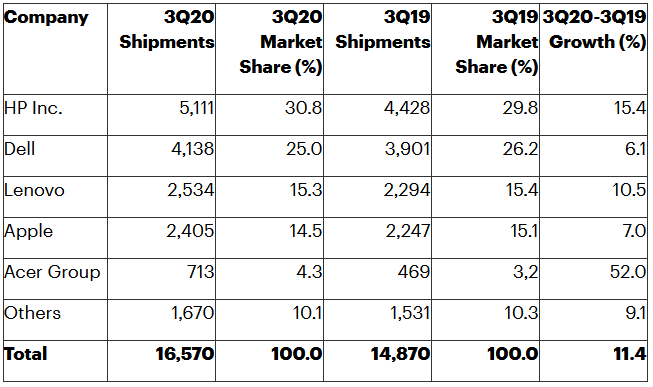

The U.S. market had a particularly strong quarter with 11.4% growth year over year, which is the first time in ten years that the region has seen double-digit growth. Robust mobile PC growth of 29% year over year was offset by a major decline in desktop PC sales.

“Mobile PC demand in the U.S. market surged as the shift from desktop to mobile PCs became a common practice across public and private businesses, even with many companies partially bringing their workers back to the office,” said Ms. Kitagawa. “PC demands in the U.S. were also backed by the gradual economic recovery throughout the quarter, including a rebound in employment and an improved consumer confidence index.”

HP secured the top spot in the U.S. PC market based on shipments with 30.8% market share. Dell followed with 25% of the U.S. PC market share (see Table 2).

Table 2. Preliminary U.S. PC Vendor Unit Shipment Estimates for 3Q20 (Thousands of Units)

Notes: Data includes desk-based PCs, notebook PCs and ultramobile premiums (such as Microsoft Surface), but not Chromebooks or iPads. All data is estimated based on a preliminary study. Final estimates will be subject to change. The statistics are based on shipments selling into channels. Numbers may not add up to totals shown due to rounding.

Source: Gartner (October 2020)

The EMEA PC market remained relatively flat in the third quarter of 2020, with just 0.4% year over year growth to 19.5 million units. The EMEA market also saw strong consumer demand for PCs, led by sales of aggressively priced notebooks for children and students as well as high-end gaming machines to support the entertainment needs of families.

Asia Pacific showed a moderate growth of 3.3% year over year, but the region showed a strong quarter over quarter growth of 16.5%, indicating a consistent recovery after a significant decline earlier in 2020. Greater China continued to show strength as the region has largely recovered from the impact of COVID-19, with public and private sectors resuming their procurement that was postponed in the first quarter of the year.

These results are preliminary. Final statistics will be available soon to clients of Gartner’s PC Quarterly Statistics Worldwide by Region program. This program offers a comprehensive and timely picture of the worldwide PC market, allowing product planning, distribution, marketing and sales organizations to keep abreast of key issues and their future implications around the globe.

Learn more about how to lead organizations through the disruption of coronavirus in the Gartner coronavirus resource center, a collection of complimentary Gartner research and webinars to help organizations respond, manage, and prepare for the rapid spread and global impact of COVID-19.

About Gartner

Gartner, Inc. (NYSE: IT) is the world’s leading research and advisory company and a member of the S&P 500. We equip business leaders with indispensable insights, advice and tools to achieve their mission-critical priorities today and build the successful organizations of tomorrow.

Our unmatched combination of expert-led, practitioner-sourced and data-driven research steers clients toward the right decisions on the issues that matter most. We are a trusted advisor and an objective resource for more than 14,000 enterprises in more than 100 countries — across all major functions, in every industry and enterprise size.

To learn more about how we help decision makers fuel the future of business, visit gartner.com.